Introduction

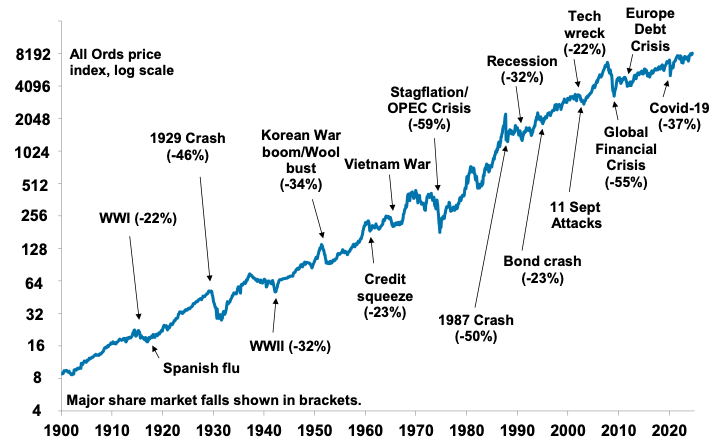

It’s often said that shares climb a wall of worry. And with good reason. The next chart shows the Australian All Ords price index since 1900 and despite wars, pandemics, and economic calamities, it’s managed to pick itself up and move on to new highs providing solid long term returns for investors.

Australian shares climb a wall of worry

Source: ASX, Bloomberg, AMP

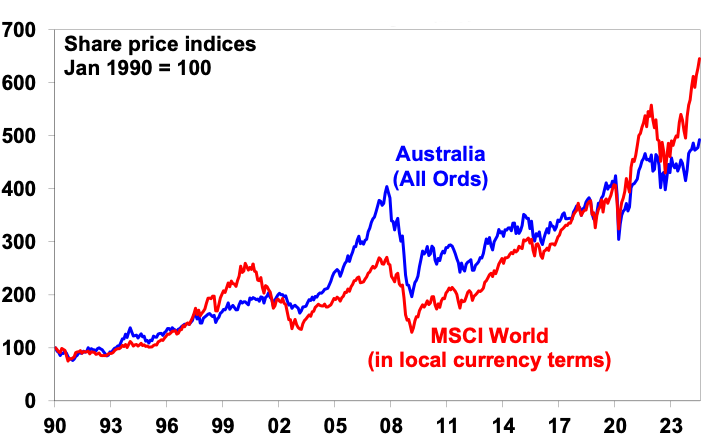

Shares have certainly climbed a wall of worry lately. Despite numerous concerns about the economic and interest rate outlook, valuations, concerns that enthusiasm for AI may be excessive and geopolitics, global and Australian shares have made new record highs. See the next chart. This has seen the Australian ASX 200 burst through its March record high of 7897 and then the 8000 level, after being below 7000 just last November.

Of course there is no particular significance in the 8000 level, being largely a function of the base date when the share market index was started and at what level making it a rather arbitrary line in the sand. But there is a psychological significance to going through big round numbers which can be referred to as “roundaphobia”, which can have the effect of attracting investor interest to it, possibly serving to push it even higher. The big question though is whether it’s sustainable? The historical experience suggests that it is, if seen as just part of the market’s rising trend over the long term and so it’s nothing remarkable. But what about over the next year?

Australian and global shares

Source: Bloomberg, AMP

Why the strength?

Three related factors have driven the Australian share market above the 8000 level. First, there is renewed optimism about interest rate cuts from the Fed. After hot March quarter inflation data which saw US rate cut expectations cut drastically and talk of possible rate hikes, US inflation has turned down again seeing renewed confidence the Fed will soon cut rates. A US rate cut is now fully priced in for September with nearly three cuts priced in by year end. This follows cuts in Switzerland, Sweden, Canada and Europe. And the Reserve Bank of NZ has pivoted from talking of rate hikes back in May to now talking of rate cuts, which has been reinforced by lower June quarter inflation. Lower interest rates offer the prospect of better global growth in 2025 and they also help improve share market valuations. This has further boosted global shares, pulling Australian shares up.

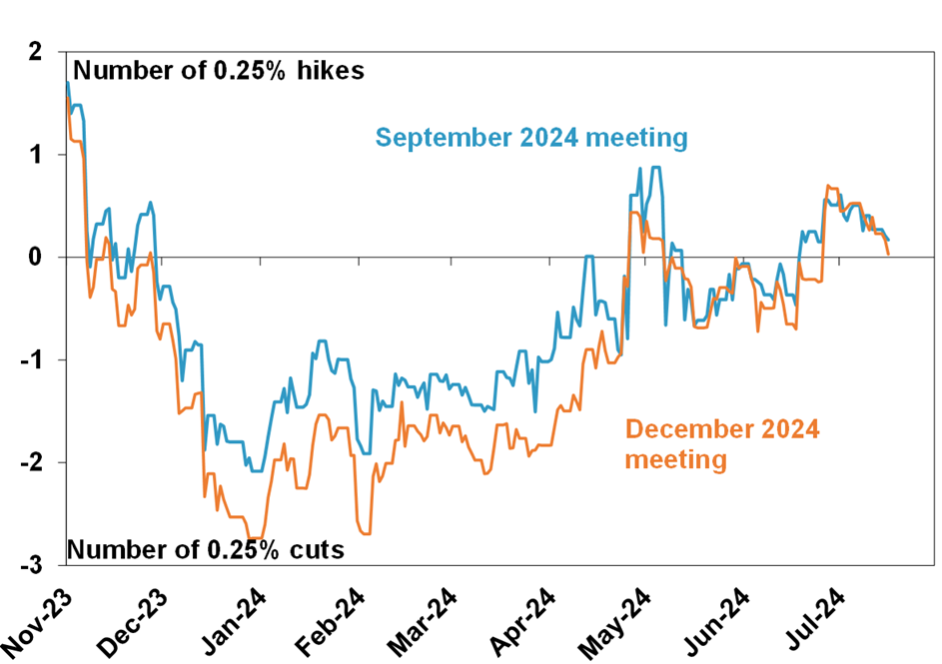

Secondly, the optimism about the Fed and the RBNZ’s pivot towards rate cuts has in turn led to optimism that the same will apply in Australia and the RBA will avoid another rate hike and head towards cuts. Consequently, we have seen money market expectations swing from around 70% probability of another hike by year end a few weeks ago to now just 16%. This has further helped boost interest sensitive Australian shares.

Number of rate RBA hikes/cuts priced in for the…

Source: Bloomberg, AMP

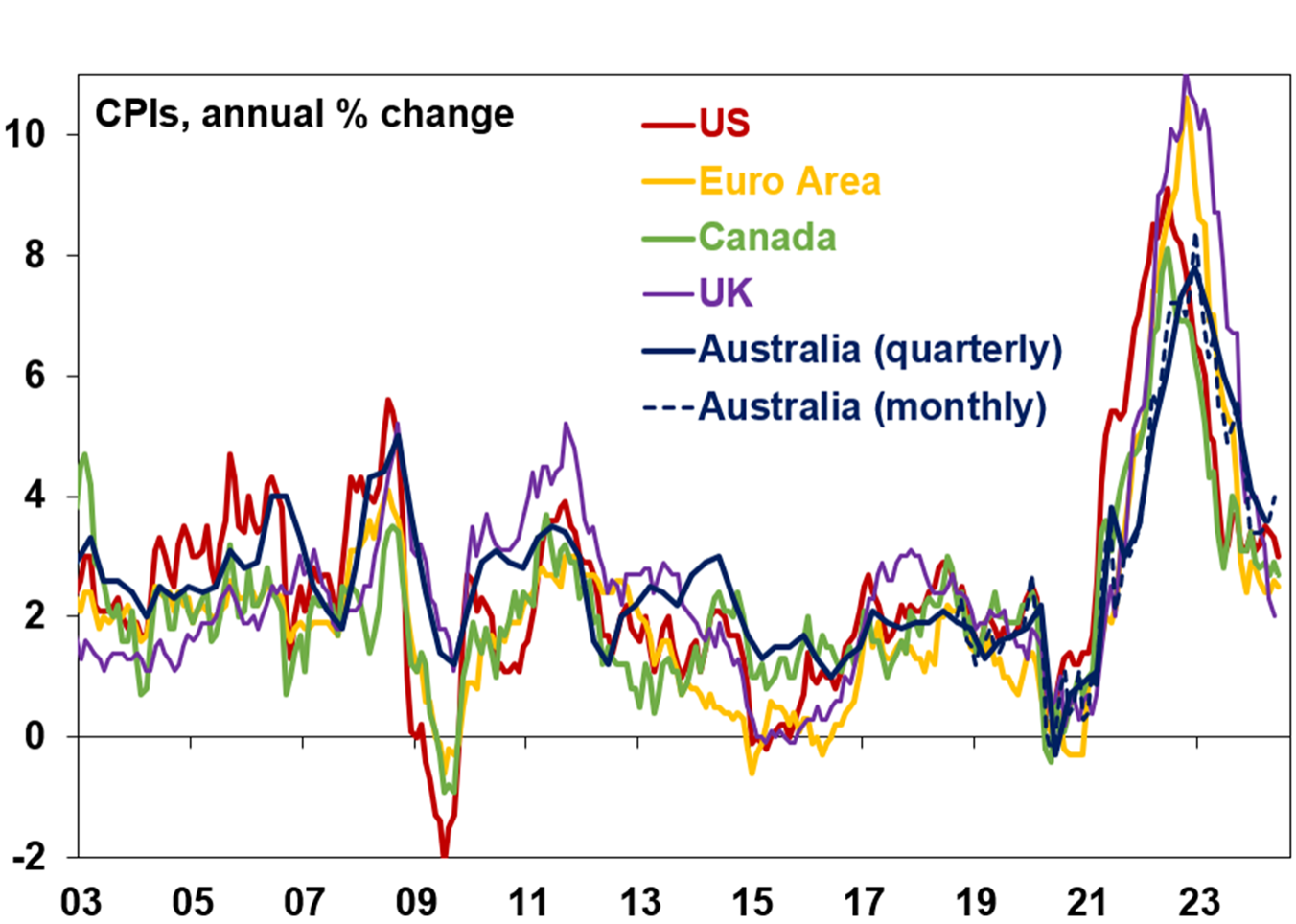

Just as Australia was part of the global upswing in inflation and rates in 2021-22 there is no reason to expect it to be different on the way down.

Global Inflation

Source: Bloomberg, AMP

Finally, there are signs of a rotation from tech shares which offer the security of high long term growth potential to value & cyclical shares which will benefit from rate cuts and any associated pickup in economic growth next year. This has been most evident in the US with a resurgence in small caps, with the Russell 2000 small cap index up more than 11% in the last week, but it may also benefit the relatively cyclical Australian share market.

Reflecting all this along with a lack of the sort of investor euphoria normally seen at major market tops, our assessment is that the Australian share market likely still has more upside on a six-to-12-month view.

Does this mean relative underperformance is over?

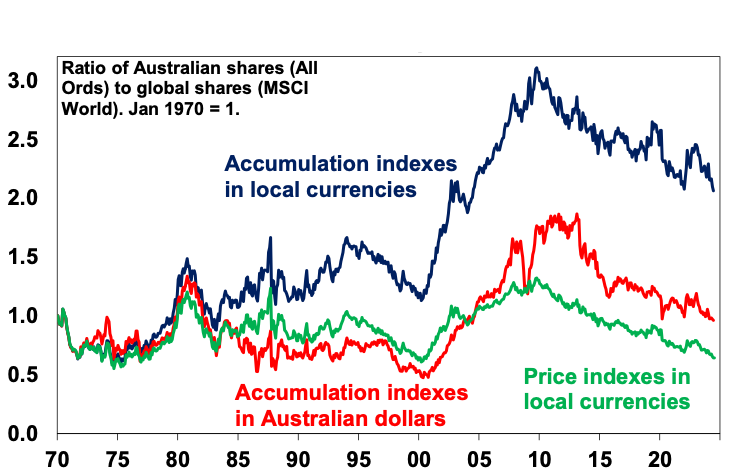

So far this year Australian shares are up 6%, which is good, but global shares are up by 16% & US shares are up by 18%. In fact, Australian shares have been underperforming since 2009. This can be seen in the next chart which compares the relative performance of Australian to global shares since 1970 in terms of: relative share prices in local currency terms (green line); relative total returns with dividends added in (blue line); and relative total returns with global shares in Australian dollars (red line).

Australian shares relative to global shares allowing for dividends and currency movements

Source: Thomson Reuters, Bloomberg, AMP

A rising ratio means Australian outperformance and vice versa. Several things stand out. First over long periods of time and when dividends are allowed for, Australian shares have had better returns than global shares when measured in local currency terms (the blue line). Since 1970 Australian shares have returned (capital growth plus dividends) 10.1% per annum compared to 8.7% pa for global shares in local currency terms. However, the falling $A over this period has enhanced the return from global shares to 10.2% pa which is roughly the same as Australian shares. Second, the swings in the relative performance of Australian shares are apparent if dividends and currency movements are allowed for or not. Since October 2009, when Australian shares peaked relative to global shares after the mining boom of the 2000s, Australian shares have underperformed returning 8.1% pa compared to 11.2% pa from global shares in local currencies or 12.7% pa in $A terms (as the $A fell).

The near 15 year period of underperformance since 2009 reflects a combination of: payback for the huge outperformance of the 2000s on the back of the mining boom; the slump in commodity prices from 2011; the lagged impact of the surge in the $A into 2011; relatively tighter monetary policy in Australia for much of the post GFC period; fear more recently that rate hikes will hit Australia harder due to more indebted households and Australia’s relatively expensive property market; worries about tensions with China and the slowing Chinese economy; and a low exposure to tech stocks – with tech stocks propelling US shares in the pandemic and more recently with AI excitement.

Some of these factors have waned – the 2000s’ outperformance has been significantly unwound, the $A is low and commodity prices appear to be in a new long-term upswing. But some still remain with regards to the relative impact of rate hikes on Australian households and the property market and the outlook for the Chinese economy and AI/tech enthusiasm could still push US and hence global shares up more than Australian shares. So having been too early in anticipating this in the last few years, it is probably too early to be confident that the underperformance is over even though Australian shares offer better medium-term prospects.

What are the main risks facing Australian shares?

There are five key risks facing the Australian share market.

-

The RBA may yet still hike again, with June quarter inflation key.

-

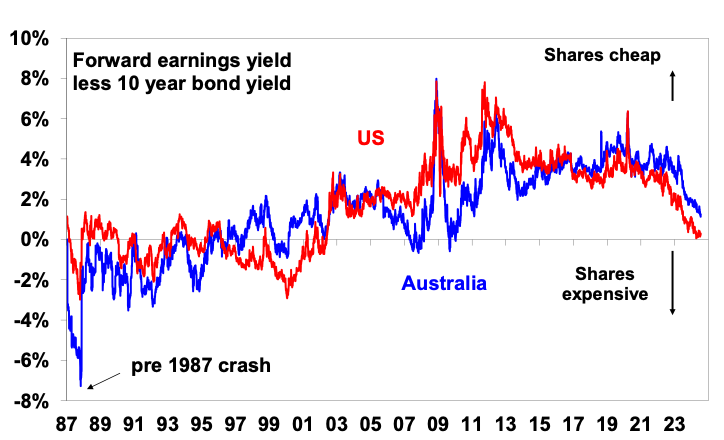

Valuations are stretched with Australian shares offering their lowest risk premium over bonds since 2010. It’s even less in the US.

Equity risk premium over bonds

Source: Bloomberg, AMP

-

The risk of recession remains high, as the full impact of rate hikes is yet to show up due to normal lags and as the economy has been protected to some degree by pandemic savings buffers.

-

Risks around the Chinese economy (which takes around 35% of our exports) remain high, with recent indicators showing growth slowing. Policy stimulus could quickly reverse this risk though.

-

Geopolitical risk is high – in particular betting markets now put Trump’s chance of winning at 67% at a time when his policies threaten a new trade war far bigger than that seen in 2018 which would threaten global growth and potentially boost inflation. As a small trading nation Australia would be vulnerable.

Concluding comment

The bottom line is that we have revised up our year-end target for the ASX 200 to 8100 (from 7900) reflecting prospects for lower interest rates globally and eventually in Australia boosting the 2025 growth outlook, but in view of the risks around valuations, near term growth and geopolitics, we are not yet prepared to go further. We anticipate a more volatile and constrained outlook with a high risk of a correction in the seasonally weak August/September period, particularly if investors start to factor in the potentially more negative economic implications for a Trump victory.

Dr Shane Oliver – Head of Investment Strategy and Chief Economist, AMP

Source: AMP Capital July 2024

Important note: While every care has been taken in the preparation of this document, AMP Capital Investors Limited (ABN 59 001 777 591, AFSL 232497) and AMP Capital Funds Management Limited (ABN 15 159 557 721, AFSL 426455) make no representations or warranties as to the accuracy or completeness of any statement in it including, without limitation, any forecasts. Past performance is not a reliable indicator of future performance. This document has been prepared for the purpose of providing general information, without taking account of any particular investor’s objectives, financial situation or needs. An investor should, before making any investment decisions, consider the appropriateness of the information in this document, and seek professional advice, having regard to the investor’s objectives, financial situation and needs. This document is solely for the use of the party to whom it is provided.